Application for Membership

GRAR Offers Several Classifications of Membership

Please Select the Appropriate Class Below

REALTOR® Member

If you are a licensed salesperson and/or a licensed/certified appraiser, complete the online application to join GRAR.

You must have a current real estate license and a sponsoring real estate broker. You will be asked to upload a PDF copy of your real estate license and along with your application. You will also be asked to pay the application fee at the time of application.

Once your application has been approved by GRAR and your broker, we will send an invoice for your pro-rated association dues and MLS fee.

Designated REALTOR®

If you are a new broker/owner and would like to join GRAR, complete this PDF application.

You must have a current real estate broker’s license. You will be asked to submit a PDF copy of your real estate license along with your application.

Secondary Member

If you are a Primary Member in another REALTOR® Association, complete this PDF application to join GRAR as a Secondary Member.

You must have a current real estate license and a sponsoring real estate broker who is a member of GRAR. You will be asked to submit a PDF copy of your real estate license along with your application.

Affiliate

Drive your business forward through the reach of GRAR’s Real Estate Professionals.

If you are engaged in the real estate profession or provide services to the real estate profession or local housing market, but not a licensed real estate salesperson or broker, we’d love to have you join our organization as an Affiliate Member.

With five membership tiers, GRAR has the membership to meet your business goal.

To join, please fill out and email this fillable PDF application to MemberServices@grar.net

If you’d like to apply in person, please schedule an appointment with our Member Services Department at GRARHelpDesk@grar.net or 585-292-5000.

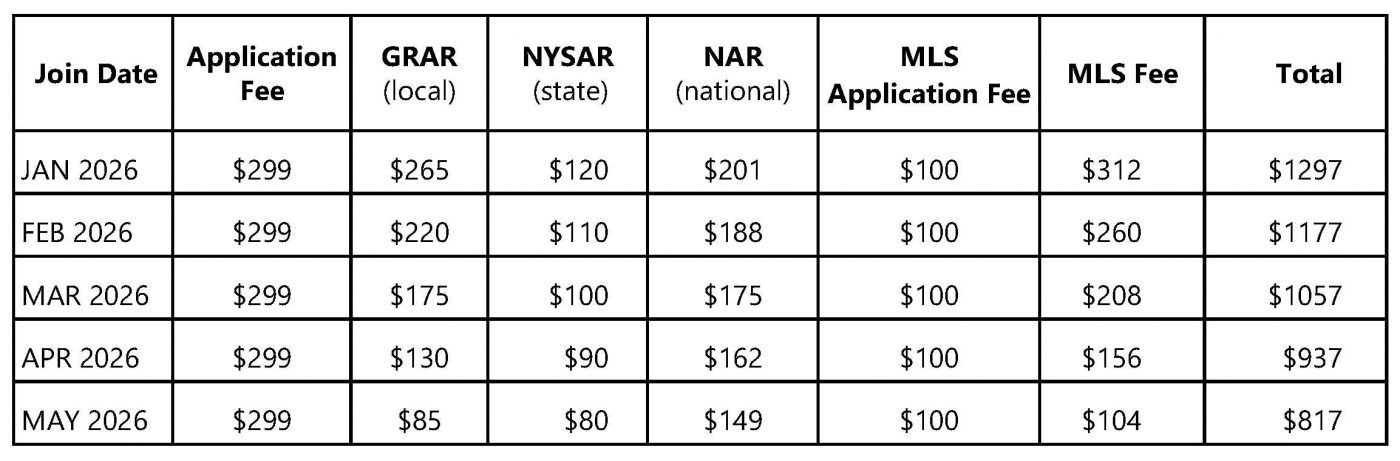

Annual Dues and Fees

GRAR is proud to offer industry-leading service and support at rates that are among the lowest in the state. All rates are pro-rated based on the month you join. Once paid, all GRAR dues are non-refundable. In recognition of their service, GRAR will waive dues for all military personnel during the time of their active deployment.

Dues and fees are pro-rated for the remainder of the time between your join date and the end of our billing cycle (June 30th). See the chart below for current year dues and fees, and contact our Member Services team with additional questions at 585-292-5000 or GRARHelpDesk@grar.net.